Business Banking

Real estate activity in St. Louis remains sound with the residential market continuing to be a “seller’s market” and multi-family properties reporting strong fundamentals. Both property types entered the pandemic on solid footing. Combined with historically low interest rates along with changing consumer preferences and in some cases, assistance through stimulus legislation, the residential and multi-family markets continue to report positive momentum.

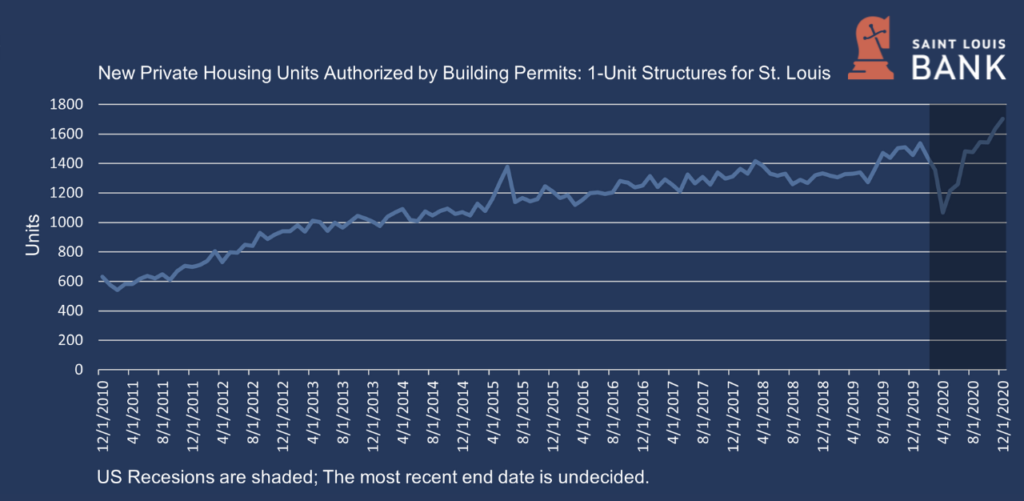

The residential housing market has proved resilient, with home sales and new construction reaching decade highs amid historically low mortgage rates. As shown on the chart below, construction activity has risen during the pandemic, with December 2020 new housing permit levels in the St. Louis MO-IL MSA at a ten-year high. This increased significantly from the “pandemic low” reported in May 2020.

This series represents the total number of building permits for 1-unit structure types. The 1-unit structure type is a single-family home or house. Single-family home or house types include fully detached, semi-detached (including side-by-side), row houses, and townhouses. Shading indicates U.S. recessions; the most recent is ongoing.

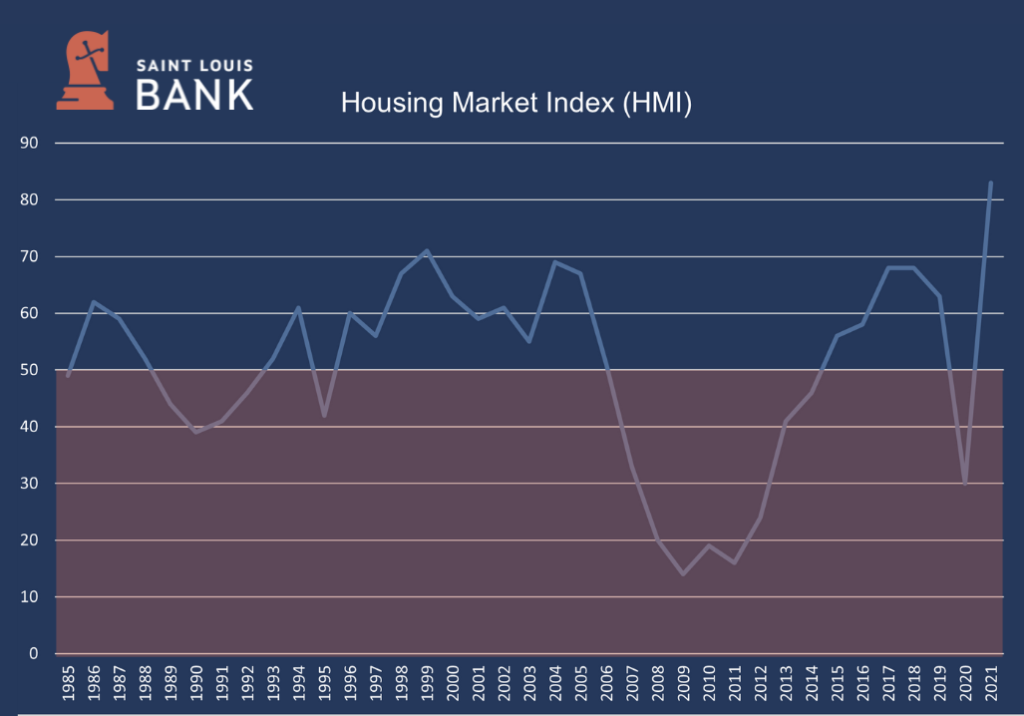

The following chart shows the Housing Market Index (HMI), also known as builder’s confidence, and is a gauge of builder opinion on the relative level of current and future single-family home sales. A reading above 50 indicates a favorable outlook on home sales; below 50 indicates a negative outlook. The index showed a sharp decline from March 2020 to May 2020 as the world entered the COVID-19 pandemic; however, the index began a sustained rebound in June 2020. The April 2021 level was 83, down 7 points from the November 2020 historic high reading of 90. Housing demand remains strong; however, the coming year may see housing affordability challenges as inventory remains low and construction costs are rising. The supply chain for residential construction is tight, particularly regarding the cost and availability of lumber, appliances, and other building materials.

Demand in 2021 is expected to be fueled by buyers who delayed purchasing homes because of the pandemic; from existing homeowners who seek larger spaces to accommodate parents working from home and children attending school virtually, to apartment and condo dwellers seeking more space. There is widespread anecdotal evidence that the pandemic shifted consumer demand from core city centers to lower-density markets, like the suburbs. Affordability has worsened in much of the United States as median home prices were up at least 10% in most of the U.S. However, low interest rates have given buyers increased purchasing power. According to Freddie Mac, the average loan commitment rate for a 30-year conventional, fixed-rate mortgage was 3.08% in March 2021, up from 2.81% in February 2021. The average loan commitment rate across all of 2020 was 3.11%. A rising rate environment would add to affordability concerns and may counteract some of the current activity in the residential market.

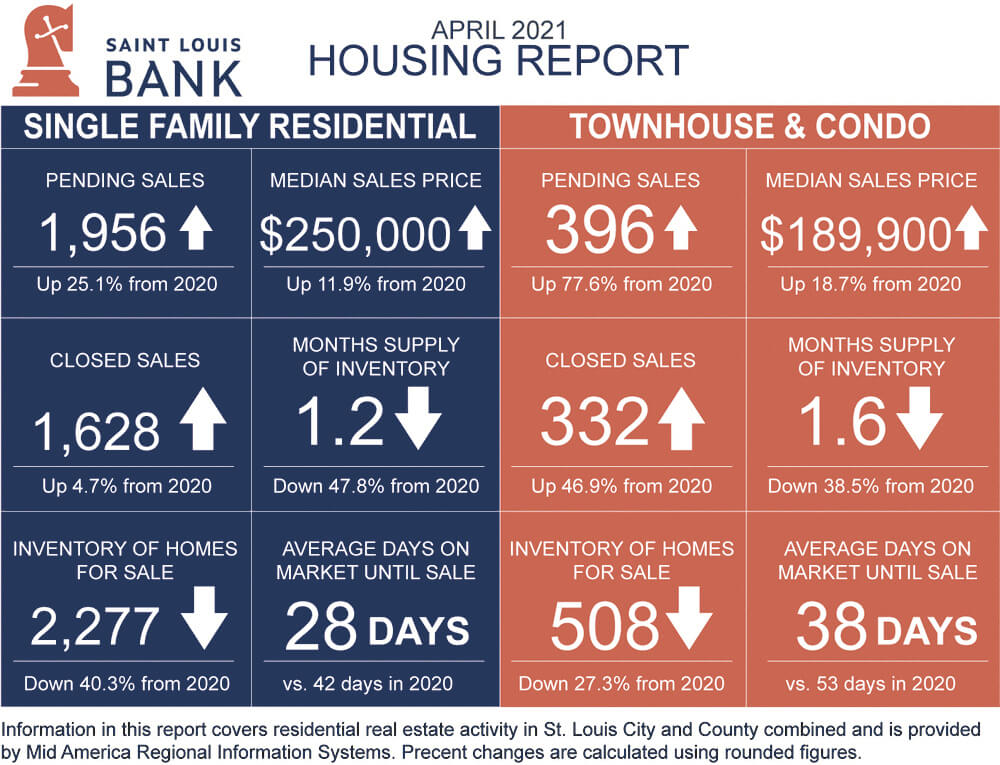

The following data is from the St. Louis REALTORS® reflecting residential activity as of April 2021. As shown, sales activity has been strong with pending sales increasing significantly from 2020. The median sales price is up 11.9% from 2020 at $250,000 for residential homes, and up 18.7% to $189,900 for townhouse and condo properties. Month’s supply of inventory decreased 48% for residential homes and 39% for townhouse and condo homes. Inventory of homes for sale was down 40.3% from 2020 and down 27.3% for townhomes and condos. Reports of multiple offer situations driving sales prices above the asking price have become more frequent. With inventory remaining constrained in most market segments, sellers continue to benefit from the tight market conditions. At the same time, buyers are faced with stress and frustration as they are frequently having to submit offers on multiple properties before they are able to secure a purchase.

The St. Louis multi-family market posted mostly steady performance throughout much of 2020, before operating conditions softened during the fourth quarter. After creeping lower in both 2018 and 2019, vacancy rose in the second half of the year. Despite the recent uptick, the current rate is consistent with the market average over the past few years.

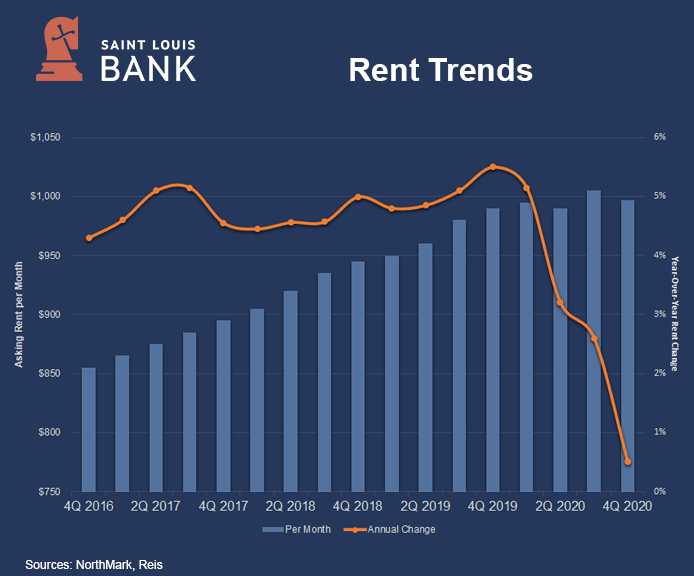

The vacancy rate in Class A properties rose during the second half of the year as new projects came online. Class A vacancy rate rose 100 basis points in the second half of 2020, reaching 7.4%. During the first half of 2020, vacancy in Class A properties inched up just 10 basis points. With apartment construction expected to accelerate in 2021, the local vacancy rate will likely trend higher. Vacancy is forecast to rise 50 basis points, ending the year at 5.6%. After several years of steady growth, rents ticked higher for most of 2020 as well, ending the fourth quarter at an average asking rent of $997 per month. Asking rents retreated slightly during the fourth quarter but still posted a modest annual gain in 2020. The pace of rent growth should accelerate in 2021 as the economy more fully reopens and businesses bring back workers. Rents in Class A units have been on an upward trajectory in recent years as newer properties have been coming to the market and have successfully leased up. After annual growth of 5% or more in each of the past four years, Class A asking rents inched up 0.2% in 2020, ending the year at $1,320 per month.

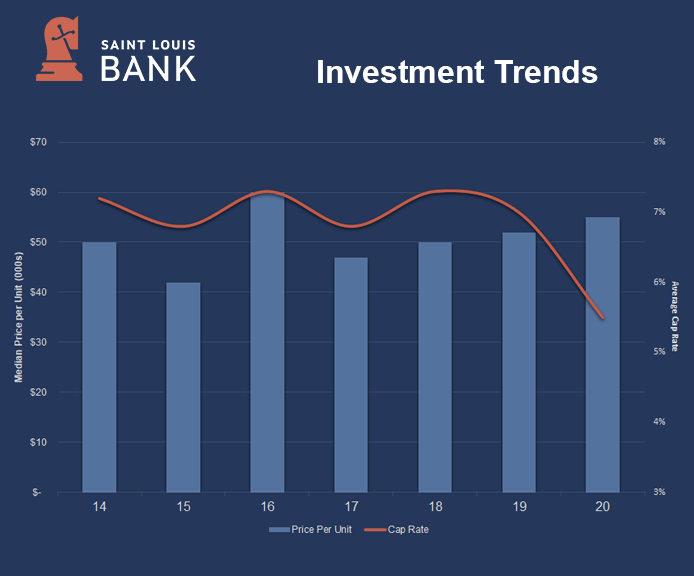

After a sluggish start to the year, the local multifamily investment market returned to fairly normalized conditions by the fourth quarter. The investment climate by the end of 2020 closely tracked trends from one year earlier, despite a turbulent year in the economy. For the full year, prices rose, and cap rates compressed into the mid-5 percent range. While the median price rose, there was a wide range of per-unit pricing. There were a few Class A properties that traded in 2020, and the median price for top-tier properties topped $270,000 per unit. At the other end of the pricing spectrum, several older Class C buildings sold at less than $30,000 per unit.

Apartment deliveries were concentrated in the second half of 2020. During the second half, projects totaling approximately 1,000 units came online, including the completion of more than 200 units in the fourth quarter. Construction activity in the second half of 2020 was up 6% from levels in the second half of 2019. Projects totaling approximately 3,100 units were under construction at the end of 2020. More than 1,400 units are under construction within the St. Louis City limits with an additional 550 units under construction in O’Fallon in St. Charles County. Permit activity accelerated during the fourth quarter, with developers pulling permits for more than 700 multifamily units during the final three months of the year. In 2020, permits for approximately 2,000 multifamily units were issued, up 34% from one year earlier.

The St. Louis multifamily market is expected to remain in a bit of a supply-demand imbalance in 2021. Employers are forecast to continue to rebuild payrolls, which should stabilize demand for apartment units. Absorption is forecast to be positive in 2021, and renters will likely move into a greater number of units than they did in 2020 when the rate slowed considerably from the two prior years. While demand will pick up, developers are on pace to bring approximately 2,000 new units to the market, a number that is expected to exceed new renter move-ins. Additionally, some concern is noted on Class C properties as high unemployment among lower wage earners is a burden on Class C demand, though the segment was resilient in 2020. Expanded unemployment benefits, rental assistance, and eviction moratoriums are helping bolster rent collections and Class C fundamentals, but challenges remain evident amid jobless claims.

Despite the disruptions of 2020, the multifamily market on a national basis is expected to see improving conditions through 2021. The year will not be easy, with unemployment remaining high and rents in the largest markets expected to remain depressed during the year. The vacancy rate is also expected to increase nationally, but significant rent declines are expected to flatten, and more markets are expected to see rent increases than not. With the rolling out of vaccines and additional stimulus legislation, the job market should rebound throughout the year, leading to greater housing demand. All in all, the long-term fundamentals of multifamily housing are still on solid ground and demographics favoring rental housing point to sustained long-term demand.

Data Sources: FRED Economic Data; St. Louis REALTORS® Housing Report – April 2021; NorthMarq Greater St. Louis Multifamily Market Report – 4Q2020; National Association of Home Builders, Freddie Mac Multifamily 2021 Outlook.

Disclaimer: The views and opinions expressed are those of the authors and do not necessarily reflect the official policy or position of Saint Louis Bank. Any assumptions made in the analysis are not reflective of the position of any other entity other than the author(s), and since we are critically-thinking human beings, these views are always subject to change, revision, and rethinking at any time. The information contained within has been obtained from sources we believe to be reliable; however, we have not conducted any investigation regarding these matters and make no warranty or representation whatsoever regarding the accuracy or completeness of the information provided. While we do not doubt its accuracy, we have not verified it nor make any guarantee, warranty or representation of any kind or nature about it. The use of or reliance upon and resource provided is a tacit acceptance that the reader understands that the materials may be out of date, opinion-based, incorrect, or biased. It is the reader’s responsibility to verify their own facts.

St. Louis Bank is an Equal Housing Lender and Member FDIC.