Business Banking

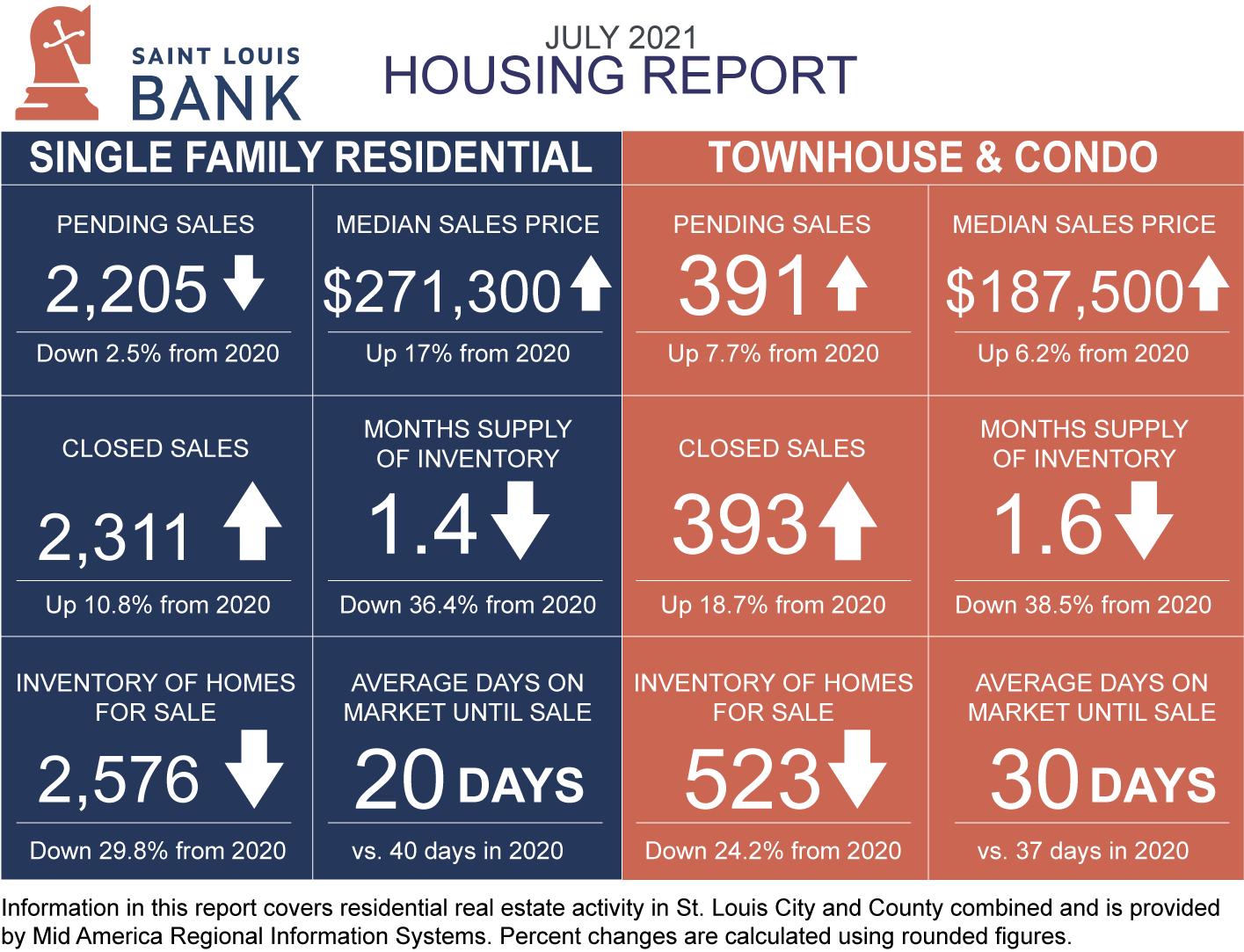

Affordability has worsened in much of the United States as median home prices were up at least 10% from last year. In the Saint Louis area, the median sales price of a single-family home was up over 11% from 2020. While the current low-interest-rate environment has given buyers more purchasing power; a bump in interest rates could slow the current momentum.

The following data, from the St. Louis Realtors Association®, reflects residential activity as of July 2021. As shown below, the median sales price is up 11% from 2020 to $272,000 for residential homes, and up 9.7% to $195,800 for townhouse/condo properties. A month’s supply of inventory decreased 27.3% for residential homes and 42.9% for townhouse/condo homes. Inventory of homes for sale was down 21.7% from 2020 and down 27.2% for townhomes and condos. Days on market averaged 21 days for residential homes vs. 36 days in 2020. With inventory remaining constrained in most market segments, sellers continue to benefit from the tight market conditions.

Sources: NorthMarq, Reis

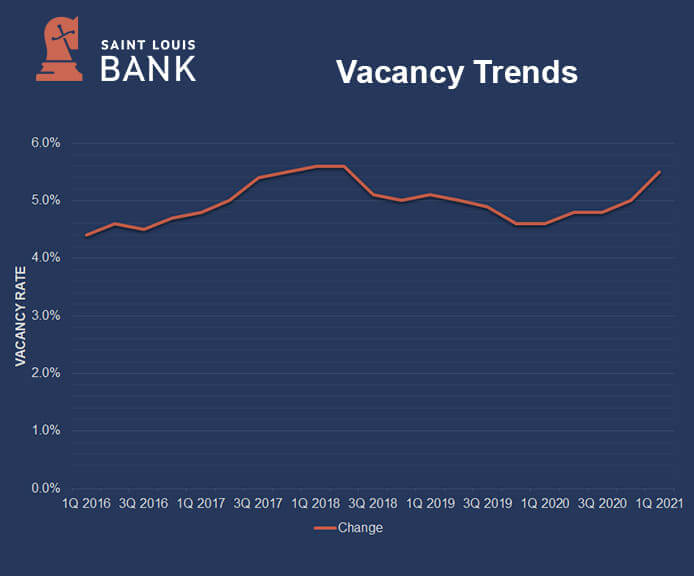

The St. Louis multi-family market posted somewhat softer conditions during the first quarter of 2021, with new supply growth outpacing net absorption, resulting in a modest rise in the vacancy rate. Apartment construction has averaged approximately 2,000 units per year since 2017, and net tenant move-ins have generally approached this level in recent years. The pace of absorption slowed in 2020, and that trend continued at the start of this year. Renter demand for apartments should increase as the local labor market gains momentum in the second half of the year, and rents may trend higher as demand strengthens.

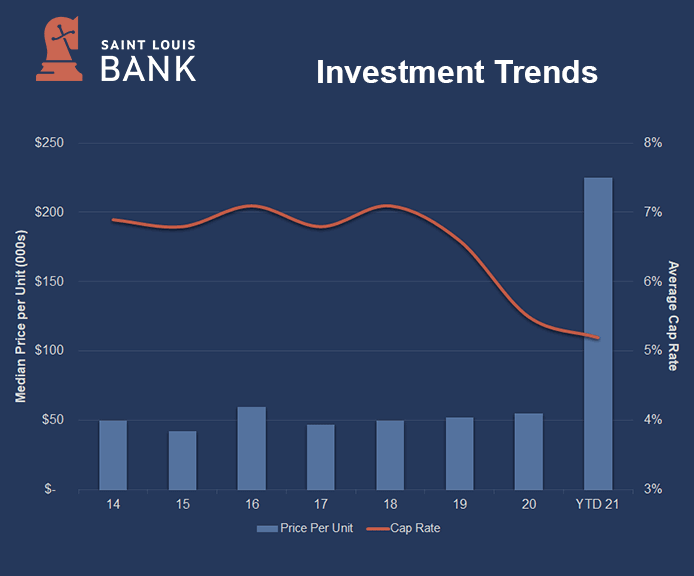

Only a handful of multifamily properties sold during the first quarter, but the assets that did change hands were at the high end of the quality spectrum and traded at prices that were significantly higher than historical ranges. Nearly all the properties that have transacted to this point in 2021 have been built within the past 10 years. In comparison, the average age of properties that sold in 2020 was approximately 45 years. With newer, Class A properties dominating the investment landscape, the median price spiked to above $225,000 per unit in the first quarter, while cap rates remained between 5% and 5.5%.

Sources: NorthMarq, CoStar, Real Capital Analytics

Apartment deliveries in St. Louis are off to a more active start to this year than in 2020. Approximately 3,500 units were under construction at the end of the first quarter of 2021, up from 3,100 units at the end of the last year. Multifamily construction activity in St. Louis is forecast to accelerate slightly in 2021, with the bulk of the units scheduled to come online by the end of the third quarter. Developers are expected to deliver approximately 2,000 new units by the end of the year.

As this year is expected to be an active one for new apartment construction, continued upward pressure on vacancy, particularly in the Class A segment of the market may persist. While the average vacancy rate in Class B and Class C properties is around 4%, the vacancy rate in Class A units is forecast to nearly double that figure. Developers are bringing units online to meet renter demand. In 2018 and 2019, absorption averaged nearly 2,600 units per year. The pace of the absorption slowed last year and could be choppy in the coming quarters before the local economy returns closer to full employment. Area investors focused on top-tier assets in their acquisitions during the first quarter, pushing prices higher as Class A properties made up the bulk of the transaction volume at the start of the year. While demand is expected to remain elevated for newer properties, particularly with several projects having been delivered and leased up in recent years, a broader mix of buildings is expected to sell in the coming quarters. Cap rates remain in a tight range, even as transaction activity was dominated by Class A deals, and cap rates are not expected to move significantly outside of current averages.

On a national level, the performance of multi-family properties has been steady with rental assistance programs offered and increased unemployment benefits. Plentiful job openings should help fund sustainable income after unemployment funds dry up. Many suburb locations experienced increased growth as people looked for increased apartments sizes during the COVID-19 pandemic. The pandemic has also seemed to fuel moves from gateway major markets to second-tier markets. Supply and demand in the St. Louis market remain generally in balance with markets such as San Francisco, Atlanta, Austin, and Indianapolis showing signs of excess supply.

——————————————————————————–

Data Sources: St. Louis REALTORS® Housing Report – July 2021; NorthMarq Greater St. Louis Multifamily Market Report – 1Q2021; Denver University – Burnes School of Real Estate & Construction Management – Real Estate Market Cycle Monitor – First Quarter 2021.

Disclaimer: The views and opinions expressed are those of the authors and do not necessarily reflect the official policy or position of Saint Louis Bank. Any assumptions made in the analysis are not reflective of the position of any other entity other than the author(s), and since we are critically-thinking human beings, these views are always subject to change, revision, and rethinking at any time. The information contained within has been obtained from sources we believe to be reliable; however, we have not conducted any investigation regarding these matters and make no warranty or representation whatsoever regarding the accuracy or completeness of the information provided. While we do not doubt its accuracy, we have not verified it nor make any guarantee, warranty or representation of any kind or nature about it. The use of or reliance upon and resource provided is a tacit acceptance that the reader understands that the materials may be out of date, opinion-based, incorrect, or biased. It is the reader’s responsibility to verify their own facts.

St. Louis Bank is an Equal Housing Lender and Member FDIC.