Business Banking

One year after the World Health Organization declared COVID-19 a global pandemic, there appears to be greater optimism about the economy, but the pandemic remains the biggest risk to both global and domestic economic growth. The economic recovery continues to depend on the ability to defeat the virus. Over the course of the past 12 months, millions of people have found themselves unemployed and trillions of dollars have gone to stimulus spending. This month’s report summarizes some key data of the past year and may provide insight as to where the economy could head next. Some of these numbers are staggering.

The above information summarizes only 10 key data points. There are other issues that will affect national and local economic conditions including potential changes in the taxation of corporations and individuals, and vaccine efficacy and distribution in different parts of the world. As we review some of the fundamentals above, we continue to believe there is a heightened risk level as we navigate through the pandemic.

On a regional basis, the pace of activity continues to remain mixed across sectors. Per research provided by the Federal Reserve Bank’s, Beige Book, published in February 2021, firms reported mixed changes in employment levels with difficulties attracting candidates for positions despite increasing wages. Inflation pressures have increased as the FRB reported moderate increases in prices, with many firms believing it will be difficult to pass on further price increases. Per the publication, which covers the Eighth District that includes St. Louis, Little Rock, Louisville and Memphis, the overall outlook continued to improve and was generally optimistic. However, most FRB contacts cited a high degree of uncertainty about the pace of recovery, which related primarily to the pace and efficacy of vaccinations.

On net, 12% of respondents to the FRB reported employment levels lower than a year ago. Contacts noted stagnant or declining employment, especially among small businesses and leisure and hospitality firms, with continuing closures in a slower-than-expected recovery. Transportation and manufacturing firms reported their desire to expand their workforce has been stymied by a scarcity of workers. Many FRB contacts ascribed this scarcity to unemployment benefits and other government aid. Some reported turning to automation. COVID-19 exposure has also depressed existing workers’ hours. Wages grew slightly. On net, 23% of FRB respondents reported wages higher than a year ago. Many contacts emphasized the need to raise wages while workers remained scarce; some, however, reported more stagnant wages, especially in the worst-hit sectors.

FRB contacts believe they have less ability to further increase prices. Some examples of this are a regional grocer reporting lowering some prices due to competitive pressures and making up profits on higher volumes, and a restaurant reporting an inability to increase prices amid already slow business. FRB contacts also noted that ocean freight costs have more than doubled, which a warehouse contact believes will lead to higher prices for consumers. Contacts also reported higher steel and lumber prices, which will impact construction projects, along with various other industries including manufacturing.

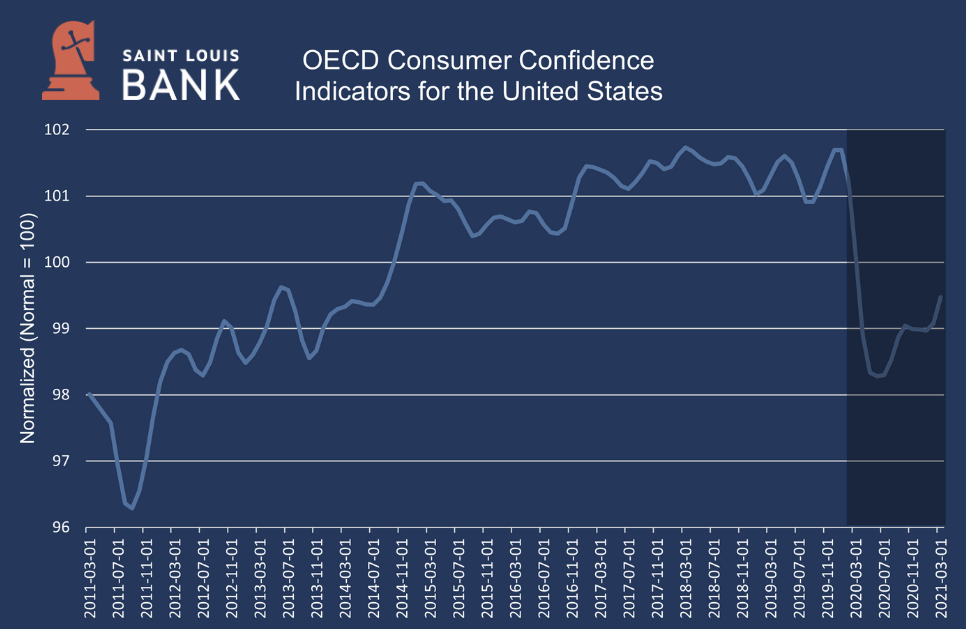

As illustrated below, consumer confidence declined sharply at the start of the pandemic. In mid-2020, we began to see recovery of this element of the economy.

Indication of consumer confidence from the Organization for Economic Co-operation and Development. Shading indicates U.S. recessions, the most recent one is ongoing.

Half of all nonfinancial services FRB contacts reported sales below expectations this quarter, reflecting clients who are cautious to spend due to uncertainty about the near-term economic recovery, as well as pandemic-related difficulties meeting new clients. Revenues at several small regional colleges have fallen due to declines in enrollment. Logistics contacts reported first-quarter sales were stronger than expected despite the post-holiday slowdown. Most contacts expect sales next quarter to be at least as good as this quarter, given vaccinations are becoming more widespread.

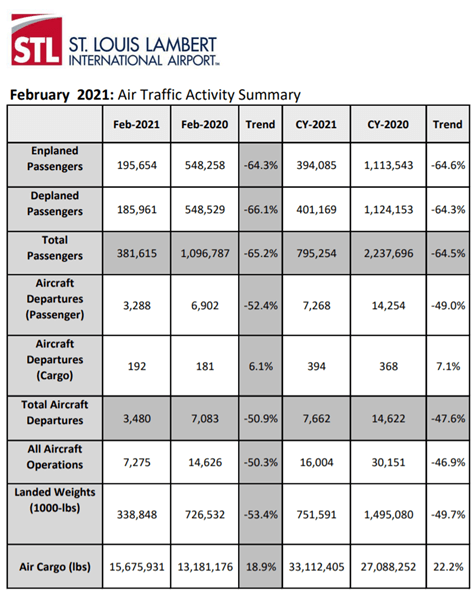

Provided below is the monthly and annual comparison of air traffic as of February 2021 at the St. Louis Lambert International Airport evidencing over a 60% decline in passenger volume. Nonetheless, the volume of air cargo has grown over 20% (in lbs.) year-over-year.

FRB contacts reported that home inventory remains low and expect it to remain so. Residential construction activity has risen this quarter, with many expecting further increases. The FRB noted that throughout the Eighth District there were some reports of residential construction projects being backlogged due to labor and material shortages. FRB contacts also reported problems and price increases stemming from high lumber and steel prices. Also, shipping delays and production issues have increased lead times on most building supplies and appliances.

Office and retail demand are lower this quarter. While the increase in telework has decreased demand for office space, going forward, there remains uncertainty if and how telework will continue to impact demand. Meanwhile, demand for industrial properties is up due to e-commerce and micro-fulfillment facilities. Commercial construction is similarly mixed, as multi-family projects, warehouses, and logistics facilities are the main projects currently being built.

The number of acres of winter wheat planted this season throughout the District increased sharply relative to the previous year. Despite pessimism in early 2020, farmers expressed optimism after a strong finish in 2020, with prices and sales up well above what was expected.

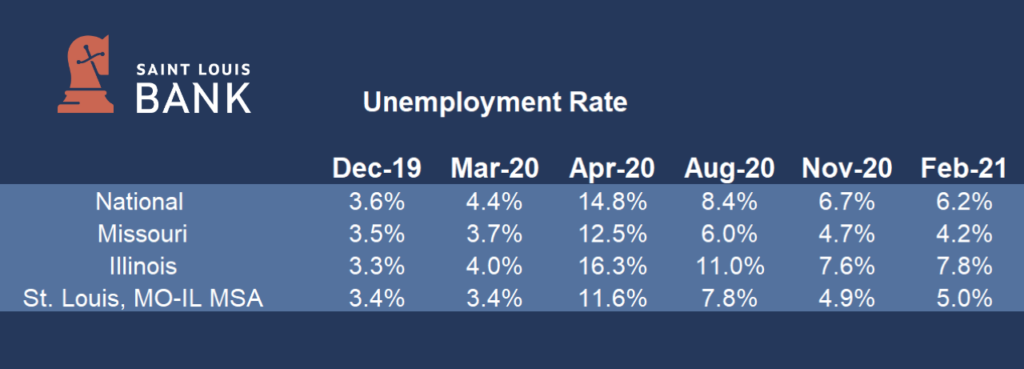

As of February 2021, the unemployment rate continues to improve with reductions nationally and in the State of Missouri. Unemployment levels in Illinois and the St. Louis MSA would generally be considered stable from the November 2020 reporting period as shown below.

At the end of 2019, before anyone outside Wuhan had ever heard of the new coronavirus, many indicators pointed to a probability of the U.S. economy entering a recessionary period. The National Bureau of Economic Research announced in February 2020 that the U.S. economy was officially in a recession. It may seem obvious with double-digit unemployment and plunging economic output, but the standard definition of a recession is a “decline in economic activity that lasts more than a few months.” The U.S. economic recovery remains uneven, still down nearly 10 million jobs almost one year later. The pandemic forced the economy to contract sharply, ending the longest expansion on record. A year after the coronavirus pandemic first drove the U.S. economy into the deepest downturn in generations, high-frequency economic indicators illustrate a strong rebound – yet there is still a long way to go.

As an aside, every recession since World War II has been preceded by an inverted yield curve. An inverted yield curve has historically been reached 2 to 3 years before a U.S. recession is officially recognized. This occurs when longer-dated yields are less than shorter-dated yields. The yield curve inverted in May 2019 until mid-October 2019 returning positive thereafter. Placing all attention on this one indicator may be somewhat misplaced as relationships between economic conditions in a global environment change over time. However, it is an important aspect of the economy to closely monitor. The pandemic escalated the response, but signals were in place indicating strain well before the pandemic was officially declared.

Data Sources: The Beige Book, Eight District – February 2021; FRED Economic Data; Forbes; St. Louis Lambert International Airport 2021 YTD Air Traffic Activity Report (February)

Disclaimer: The views and opinions expressed are those of the authors and do not necessarily reflect the official policy or position of Saint Louis Bank. Any assumptions made in the analysis are not reflective of the position of any other entity other than the author(s), and since we are critically thinking human beings, these views are always subject to change, revision, and rethinking at any time. The information contained within has been obtained from sources we believe to be reliable; however, we have not conducted any investigation regarding these matters and make no warranty or representation whatsoever regarding the accuracy or completeness of the information provided. While we do not doubt its accuracy, we have not verified it nor make any guarantee, warranty, or representation of any kind or nature about it. The use of or reliance upon and resource provided is a tacit acceptance that the reader understands that the materials may be out of date, opinion-based, incorrect, or biased. It is the reader’s responsibility to verify their own facts.

St. Louis Bank is an Equal Housing Lender and Member FDIC.