Business Banking

By Rita Kuster, Chief Credit Officer, Saint Louis Bank

While many economic fundamentals remain strong, there are signals that a “pandemic boom” is starting to wane with reoccurring concerns noted regarding supply chain disruptions, inflation, labor shortages and fiscal policy. The Delta variant of COVID-19 and lingering vaccination acceptance at 57.4% of the U.S. population is resulting in a longer-lasting virus drag on virus-sensitive consumer services. That said, the Delta variant is unlikely to derail the economy as its predecessor did; however, it does cloud the near-term outlook and serves as a reminder that low-growth scenarios are a real possibility. The trajectory of the virus through this fall and winter, inflation, and fiscal policy are the most significant unknowns to consider for the upcoming months.

As you read through this report, you will find some reoccurring themes—labor shortages, rising prices, supply chain issues, and inflation concerns as well as sound manufacturing demand and residential and industrial real estate market strength. All leading to economic conditions that will continue to rapidly evolve for individuals and businesses. Highlights of some of the research are discussed below.

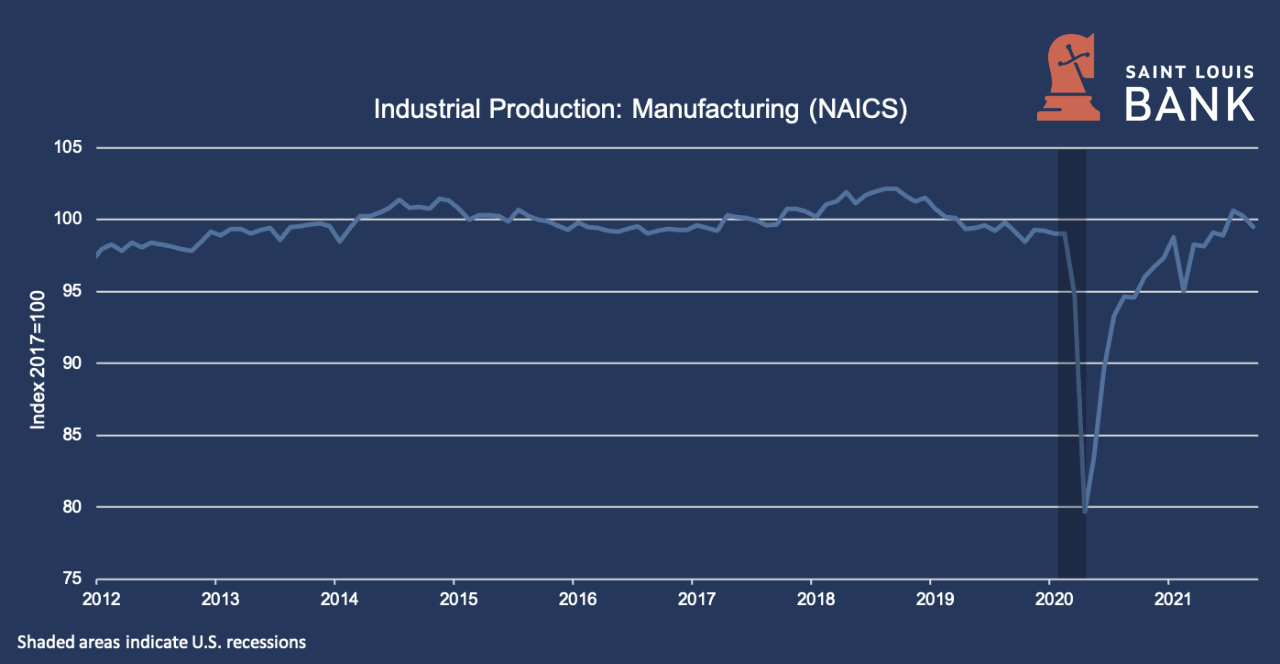

Board of Governors of the Federal Reserve System (US), Industrial Production: Manufacturing (NAICS) [IPMAN], retrieved from FRED, Federal Reserve Bank of St. Louis; October 25, 2021. Shading indicates U.S. recessions.

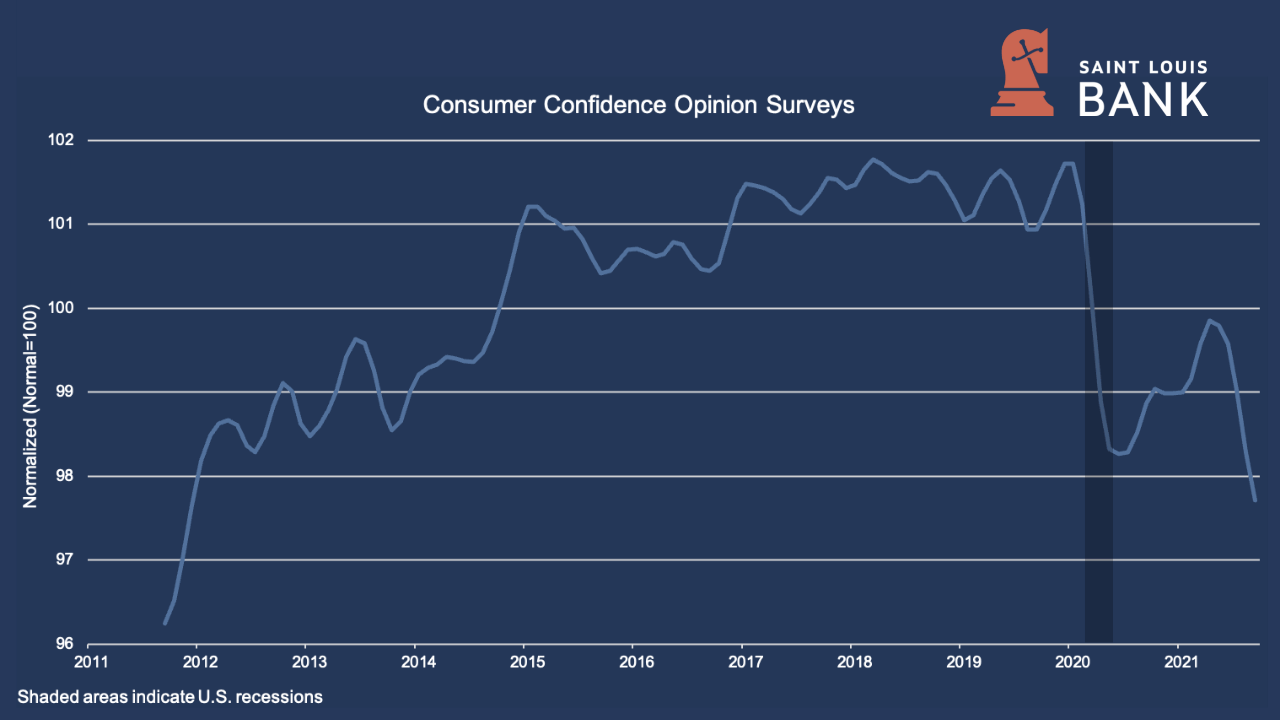

The downward trend in consumer confidence is illustrated in the following graph. The current level is at its lowest point not only since the start of the pandemic, but in nearly 10 years (since December 2011).

Organization for Economic Co-operation and Development, Consumer Opinion Surveys: Confidence Indicators: Composite Indicators: OECD Indicator for the United States [CSCICP03USM665S], retrieved from FRED, Federal Reserve Bank of St. Louis; October 25, 2021. Shading indicates U.S. recessions.

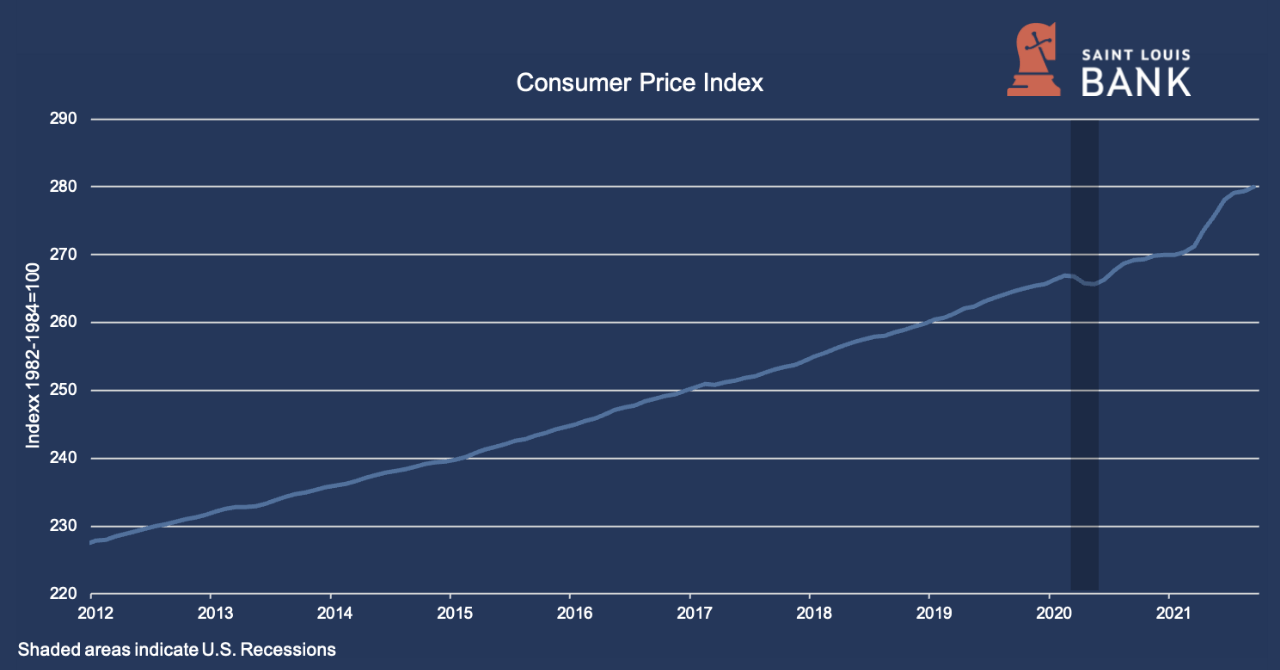

As shown on the graph below, the “Consumer Price Index for All Urban Consumers: All Items Less Food and Energy in U.S. City Average” has shown a steady increase since May 2020 with the highest level reported in the 10-year of data shown most recently. The “Consumer Price Index for All Urban Consumers: All Items Less Food & Energy” is an aggregate of prices paid by urban consumers for a typical basket of goods, excluding food and energy. This measurement, known as “Core CPI,” is widely used by economists because food and energy have very volatile prices.

The CPI can be used to recognize periods of inflation and deflation. Significant increases in the CPI within a short time frame might indicate a period of inflation, and significant decreases in CPI within a short time frame might indicate a period of deflation.

U.S. Bureau of Labor Statistics, Consumer Price Index for All Urban Consumers: All Items Less Food and Energy in U.S. City Average [CPILFESL], retrieved from FRED, Federal Reserve Bank of St. Louis; October 25, 2021. Shading indicates U.S. recessions.

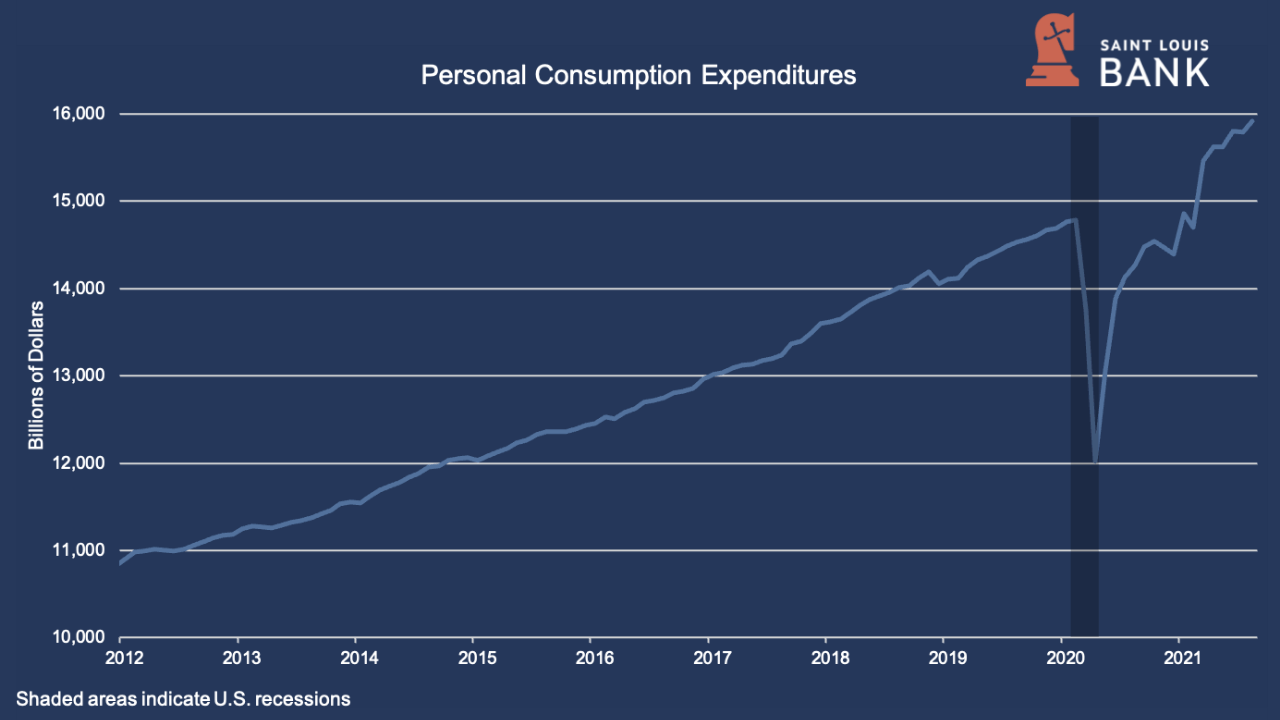

Despite the price index increasing, personal consumption expenditures have increased as well indicating that the consumer is accepting the current price trends with the highest period of expenditures in the 10-year timeframe shown in the chart below occurring recently. This could be representative of pent-up consumer demand from early in the pandemic, supported by increased personal liquidity.

U.S. Bureau of Economic Analysis, Personal Consumption Expenditures [PCE], retrieved from FRED, Federal Reserve Bank of St. Louis; October 25, 2021. Shading indicates U.S. recessions.

On a regional basis, economic conditions have continued to improve at a moderate pace per the October 2021 Eighth District Beige Book published by the Federal Reserve Bank (“FRB”). Per the publication which covers the Eighth District that includes St. Louis, Little Rock, Louisville and Memphis, labor shortages and supply chain disruptions continue to be primary issues. Increased input costs have led to cost pressures across industries, and firms with the power to do so reported passing along these costs to their customers. Consumer spending has remained steady and residential real estate inventories have increased slightly, but prices remain high. Industrial real estate continues to experience strong growth.

Employment has increased modestly, with widespread hiring attempts hindered by the continuing labor shortage. Firms responding to the Federal Reserve survey reported various strategies to attract scarce workers. Some redesigned open positions to be more attractive; others held job fairs; others turned to offshoring; and many reported sign-on and retention bonuses. Several firms emphasized a new focus on students and young workers. Other FRB contacts simply reported adapting to worker shortages—automating jobs, cutting down on business hours, and turning to contractors as necessary. Wages continued to increase strongly in the tight labor market, with small firm wages rising more slowly.

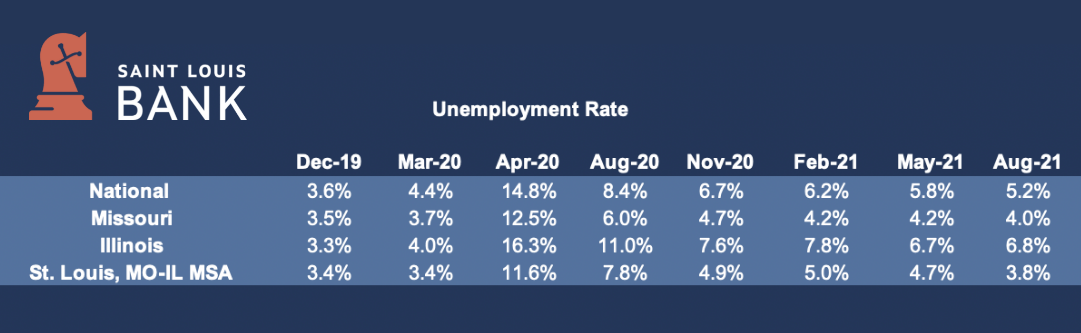

As of August 2021, the unemployment rate continues to improve with stable-to-decreasing unemployment.

Prices have increased moderately per the Federal Reserve’s report. Some industries, such as construction, have been able to pass these cost increases to consumers, whereas FRB contacts in the healthcare industry noted difficulty passing along increases in input costs. One contact noted double-digit price increases on farming equipment. In the construction industry, contacts reported lower lumber prices but noted high costs for items such as steel and shingles.

General retailers, auto dealers, and restaurants continued to report that supply chain issues and labor shortages are restraining sales. Hospitality contacts reported that revenue per available room exceeded 2019 levels in early October for the second time since the pandemic began.

Manufacturing activity has seen a moderate increase. Firms reported upticks in new orders and production, although the rate of growth has slowed slightly. Supply chain delays and availability have continued to be issues, affecting the prices of intermediate goods in steel, concrete, and timber. Manufacturers are beginning to explore producing these goods domestically to address shortages. Contacts are still optimistic about future growth but remain concerned over global supply chains and wage inflation.

Activity in the non-financial services sector has increased slightly since the last FRB report. Airport passenger traffic remains near 80% of pre-pandemic levels due to strong leisure travel; several airport contacts were optimistic about business travel as more firms return to in-person work. Several transportation contacts noted that demand is strong, but shortages of shipping containers and barges remain an issue. A healthcare contact noted that, while revenue has improved since this time last year, surgery and emergency room revenues have not returned to pre-COVID levels. Several healthcare contacts mentioned that hospitals are busy, in part due to COVID patients and are facing staffing shortages.

The residential real estate market has remained strong. Inventory remains restricted, but there are some increases in inventory across all price ranges. Prices remained steady, but there are fewer bidding wars and some price reductions. Residential construction has remained strong since the prior report, but the industry is struggling with supply chain shortages and retaining workers. Many input materials continue to have extended lead times. Some buyers who purchased a property and planned to build on it have elected to delay construction until supply chain issues are resolved.

The commercial real estate market has remained mixed since the prior report. Industrial real estate remains strong, and many major firms are buying build-to-suit and spec industrial space across the District. The office market seems to be improving, but prices and vacancy rates have not returned to pre-pandemic levels. Contacts report that companies are more willing to sign leases but are still wary of signing full five-year lease contracts. There is very little financing available for office space, which is causing delays as landlords and tenants disagree over who should pay for repairs and improvements. The market for retail space struggled last year, but demand has improved since February.

Banking conditions have worsened slightly since the prior report. FRB contacts noted a pause in lending activity due to uncertainty surrounding the Delta variant. Consumer, commercial, and industrial loans declined moderately, while real estate loans increased modestly. Delinquency rates remained low, but some lenders are concerned that delinquencies will increase as unemployment benefits have expired.

District agriculture conditions have slightly improved since the last FRB report. Overall crop yields have increased moderately over the previous year. Farmers have reported a strong harvest season combined with high prices, which have contributed to a strong season overall. However, there are concerns about rising input prices, global supply chain disruption, and the lack of labor necessary for both low- and high-skilled agriculture work.

There continue to be various aspects of the economy to watch as the COVID-19 pandemic will force structural changes that will challenge some sectors. The pandemic’s long-term impacts may take many forms, positive and negative, and will likely continue to surprise us.

At the end of 2019, before anyone outside Wuhan had ever heard of the novel coronavirus, many indicators pointed to a probability of the U.S. economy entering a recessionary period. The National Bureau of Economic Research announced in February 2020 that the U.S. economy was officially in a recession. It may seem obvious with double-digit unemployment and plunging economic output, but the standard definition of a recession is a “decline in economic activity that lasts more than a few months.” The pandemic forced the economy to contract sharply, ending a record expansion. This brought an ending to the longest expansion on record. According to the National Bureau of Economic Research, the contraction lasted just two months, from February 2020 to the following April, which makes the two-month downturn the shortest in U.S. history. Though the drop featured a staggering 31.4% GDP plunge in the second quarter of the pandemic-scarred year, it also saw a massive snapback the following period, with previously unheard-of policy stimulus boosting output by 33.4%. More than a year after the coronavirus pandemic first drove the U.S. economy into the deepest downturn in generations, many high-frequency economic indicators illustrate a strong rebound.

As an aside, every recession since World War II has been preceded by an inverted yield curve. A negative yield curve has historically been reached 2 – 3 years before a U.S. recession is officially recognized. All attention on this one indicator may be somewhat misplaced as relationships between economic conditions in a global environment change over time. However, it is an aspect of the economy to closely monitor. The pandemic escalated this response, but signals were in place indicating strain well before the pandemic was officially declared.

Data Sources: Deloitte Insights – United States Economic Forecast, 3rd Quarter 2021; 2021 Equipment Leasing & Finance U.S. Economic Outlook, Q4 Update – October; FRED Economic Data – Federal Reserve Bank of St. Louis; Federal Reserve Bank, The Beige Book, October 2021.

Disclaimer: The views and opinions expressed are those of the authors and do not necessarily reflect the official policy or position of Saint Louis Bank. Any assumptions made in the analysis are not reflective of the position of any other entity other than the author(s), and since we are critically-thinking human beings, these views are always subject to change, revision, and rethinking at any time. The information contained within has been obtained from sources we believe to be reliable; however, we have not conducted any investigation regarding these matters and make no warranty or representation whatsoever regarding the accuracy or completeness of the information provided. While we do not doubt its accuracy, we have not verified it nor make any guarantee, warranty or representation of any kind or nature about it. The use of or reliance upon and resource provided is a tacit acceptance that the reader understands that the materials may be out of date, opinion-based, incorrect, or biased. It is the reader’s responsibility to verify their own facts.

St. Louis Bank is an Equal Housing Lender and Member FDIC.