Business Banking

As always, we have separated our commercial real estate report into three sections: Industrial, Office, and Retail, to either consume the information that is most relevant to you or read fully. Each sector differs in its recovery from the COVID-19 pandemic. However, we can see a region that is continuing to adapt to a year of unparalleled circumstances.

The St. Louis industrial sector entered the pandemic on solid footings, and while there have been pockets that have been adversely affected, the industrial market has been one of the most resilient real estate sectors amid the COVID-19 pandemic. This resiliency has been largely driven by changing consumer behavior, particularly in e-commerce growth. It is anticipated that industrial space will continue to be active as customers demand rapid delivery of more products and manufacturing activity picks up.

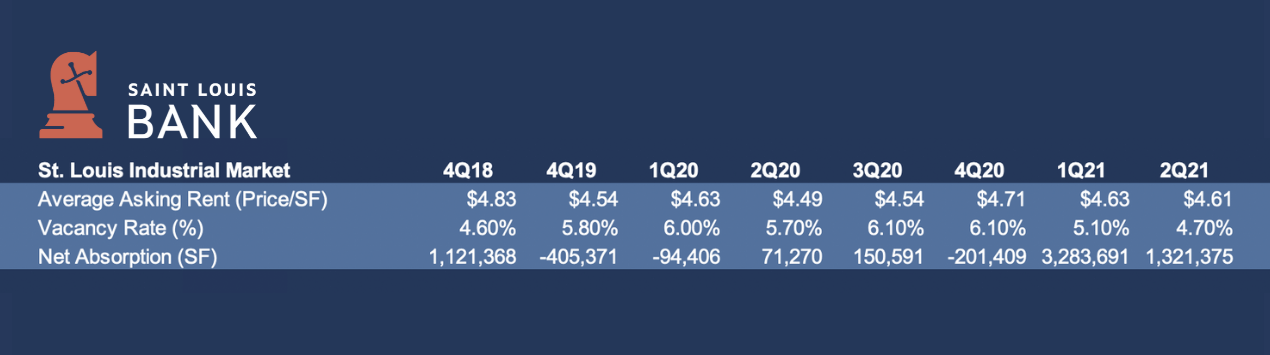

The St. Louis industrial sector tightened in the second quarter of 2021. During this period, the market realized positive absorption of 1.3 million square feet, the third highest quarterly absorption since third-quarter 2017. Overall vacancy decreased 40 basis points from the prior quarter to 4.7%, while average quoted rents slightly decreased from $4.63 per square foot to $4.61 per square foot. Seven properties, including the 252,270 square foot Hazelwood TradePort Building 1; the 142,000 square foot, fully occupied Patriot Machine building in St. Charles; and the 111,880 square foot Earth City Commerce Center located at 3930 Earth City Expressway delivered 663,560 square feet of product to the market during the quarter, while developments under construction remained at 2.7 million square feet.

The market absorbed the most space during the first half of 2021 since the second and third quarters of 2017. Net absorption totaled 5.4 million square feet for the past four quarters, equating to a 29.8% increase from the annual average net absorption of 4.2 million square feet during the previous five years. Quoted rental rates increased by $0.12 per square foot over the past year. With market vacancy at 4.7%, the following major projects are currently under construction:

The St. Louis industrial market is well-positioned for the remainder of 2021 as Midwestern industrial markets, including St. Louis, Kansas City, Memphis, Indianapolis, Nashville, and Columbus, continue to post significant net absorption and attract investor interest. Among the Midwestern industrial markets, St. Louis posted the second-lowest vacancy rate and ranked 13th in the U.S. for net absorption to total market size among the most active markets in the nation. The industrial market’s strong prevailing fundamentals, coupled with reasonable rental rates, an affordable workforce, and centralized geographic locations, will continue to attract new tenants to the metro looking to invest heavily in logistics and industrial networks. A more pronounced shift toward online retail will increase demand for warehouse and distribution space, which will increase the speed to market required by tenants.

National trends are in line with the St. Louis market as industrial transaction prices per square foot are on the rise, in addition to vacancy rates remaining low and new leases being signed at higher rates. Despite new current and planned supply being greater than it has been in years, higher demand for industrial real estate is causing net absorption to remain strong. A continued surge in imports from retailers restocking depleted inventories has exacerbated the shortage of warehouse space near major logistic hubs, highlighting the need for additional construction. Although supply chain disruptions are less severe than earlier this year, the cost of building materials remains above pre-pandemic levels, and construction workforce shortages may delay industrial completions. Strong returns on industrial real estate have continued to attract investment in the sector, contributing to higher transaction prices and additional development. There is a continued need for last-mile industrial space and cold-storage facilities, which supports a premium for properties adjacent to more densely populated areas.

The pandemic highlighted the fact that many businesses were too reliant on foreign manufacturing and importation. As manufacturers shift away from importing, these businesses will be better positioned to minimize overall supply chain issues. Since businesses cannot diversify their suppliers overnight, the demand for expansion could continue over the next three to five years, strengthening the industrial sector as businesses explore more domestic options.

The significant pandemic-driven changes to the office sector last year will carry into 2021 and beyond as companies adapt to innovative new operating models. Buildings emptied last year as companies downsized and shifted their staff to work from home. To meet health and safety standards, facility operators quickly enhanced their cleaning procedures, upgraded HVAC systems, erected plexiglass barriers, closed shared spaces, and added other physical-distancing measures to keep workers safe. Companies have become increasingly nimble, adding sophisticated remote-work capabilities. Most companies have effectively halted their office space expansion plans, shelving growth strategies until the vaccine reaches a critical mass of the population and clarity on the future of office work emerges. This may include hybrid work models driving more flexibility in office space. When able, businesses found themselves shifting toward short-term lease renewals versus trying to solve longer-term space needs amid the pandemic.

Most firms recognize there is always going to be a need for office space. However, it may be less dense and/or more flexible to accommodate hybrid work from home models. The more crucial determinant of office demand is sheer job growth.

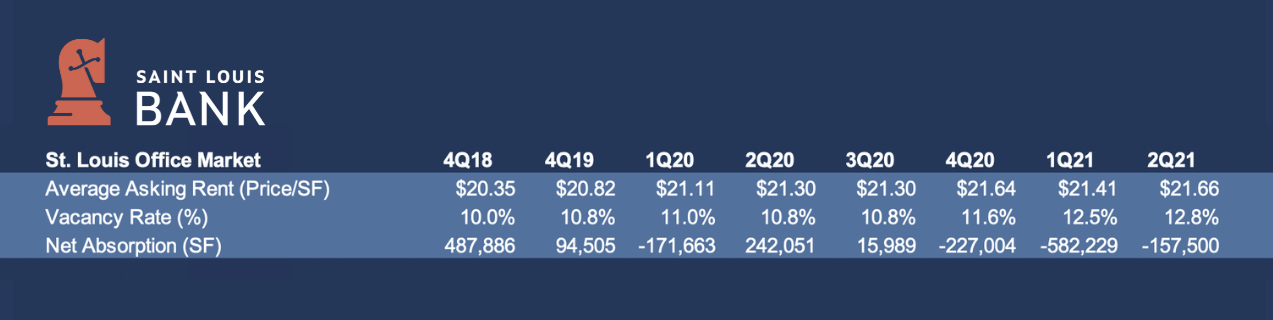

The St. Louis office market realized an increase in asking rental rates in the second quarter of 2021. Rents climbed to a record high of $21.66 per square foot, up $0.25 per square foot from the first quarter 2021. Market vacancy rose to 12.8%, an increase of 30 basis points from the prior quarter and an increase of 230 basis points from one year ago. Total net absorption in the quarter measured negative 157,500 square feet, bringing the total for the past four quarters to negative 1.7 million square feet. One construction project underway during the quarter totaled 224,585 square feet. The Class A, Forsyth Pointe project in Clayton is currently 41.7% pre-leased. No projects were delivered to the market during the quarter.

The St. Louis office market loosened in second-quarter 2021, as negative 157,500 square feet were absorbed. With net absorption during the past four quarters totaling negative 1.7 million square feet, average quarterly net absorption has significantly decreased, measuring negative 81,777 square feet during the previous two years. Leasing commitments during the quarter were active in various submarkets, increasing 61.0% from the prior quarter, as tenants locked in favorable terms for new direct and subleased spaces, as well as renewals. It is believed that these more favorable terms may be a residual impact from COVID-19 and the overall stresses on the office sector. Expect favorable conditions and opportunities for prospective tenants to upgrade from Class B or B+ space to Class A space in 2021, as most submarkets in the Metro display vacancy rates for Class A space ranging from 10.0% to 26.2%, with Class A vacancy in North County and Downtown St. Louis at market highs of 16.4% and 26.2%, respectively. Overall market vacancy should range from 12.6% to 13.6% while asking rental rates are expected to range from $21.50 per square foot to $22.35 per square foot during the next four quarters.

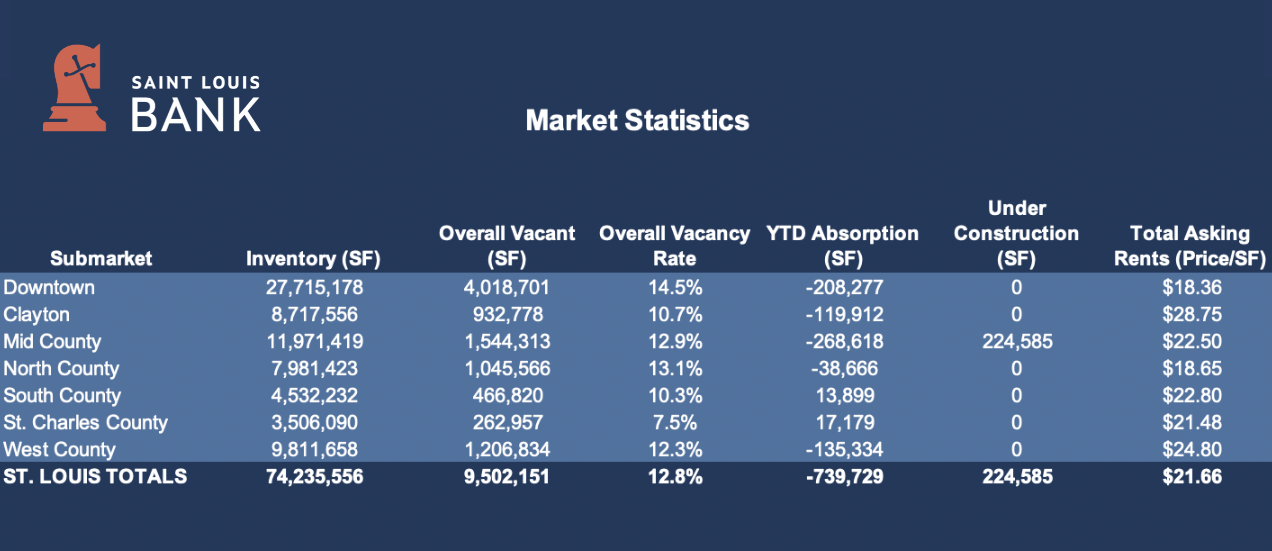

Looking further into the transactions noted above, the impact of the COVID-19 pandemic on office space and office space offerings is apparent in the St. Louis market.

On a national basis, many markets shifted to the hyper-supply phase, which exhibits increasing vacancy and slowing trends in rental rate growth. The move from high-cost “gateway” east and west coast markets to the lower cost of living, second-tier markets seem to have been accelerated by COVID-19. Further, high-quality suburban, boutique properties became more attractive as organizations look to move out of high-density urban cities into areas that may not rely as heavily on public transportation. Additionally, these suburban locations allow for easier work-from-home access because often the property is closer to where employees live. “Back to the office” plans have begun their execution with mask mandates lifted, but many firms are taking the return slowly to manage employee flex-work desires while balancing the need to build and promote culture and collaboration between colleagues. Much of this has been tempered by the Delta Variant of COVID-19, so a clear picture of post-COVID-19 office may not surface until 2022 and beyond.

As the retail sector includes numerous categories – many of which were subject to widespread government restrictions – it was undoubtedly hit hard during the pandemic. However, certain sub-sectors of retail such as grocery-anchored or necessity-based retail have proven to be resilient. The retail space is gradually returning to normal as everyone better understands and embraces safety protocols. A rapid rise in e-commerce has also presented new opportunities. Convenience has become king, and necessity-based retail accommodates that in many ways.

COVID-19 accelerated trends in the retail sector that existed before the pandemic. This is largely evidenced by the decline in enclosed shopping malls and the adoption of e-commerce. There is now an increasing demand for omnichannel retail, which offers a hybrid experience of online and brick-and-mortar shopping. This has caused businesses to rapidly rethink how to improve delivery and fulfillment options via their existing supply chains, while simultaneously driving sales via a website or app. While some shoppers still prefer to visit physical retail locations, many may prefer to pick up their goods quickly in-store or at designated curbside locations. Prior to the pandemic, e-commerce was one of the major trends influencing the retail sector and this will likely continue long after a vaccine is widespread. Nonetheless, physical stores have proven to be a very important part of the supply chain and will continue to morph and adapt to fulfill their role in a diversified supply chain. Though more people are shopping online than ever before, many consumers prefer well-positioned neighborhood shopping centers that fit into their routine traffic patterns. For some retailers, finding competitive space could also be an issue as tenants are not choosing the cheapest rent locations. Instead, retailers want the best property with bigger name co-tenants that will drive traffic. If the pandemic continues to slow the growth of new builds, the strongest – not the cheapest – locations will become most competitive.

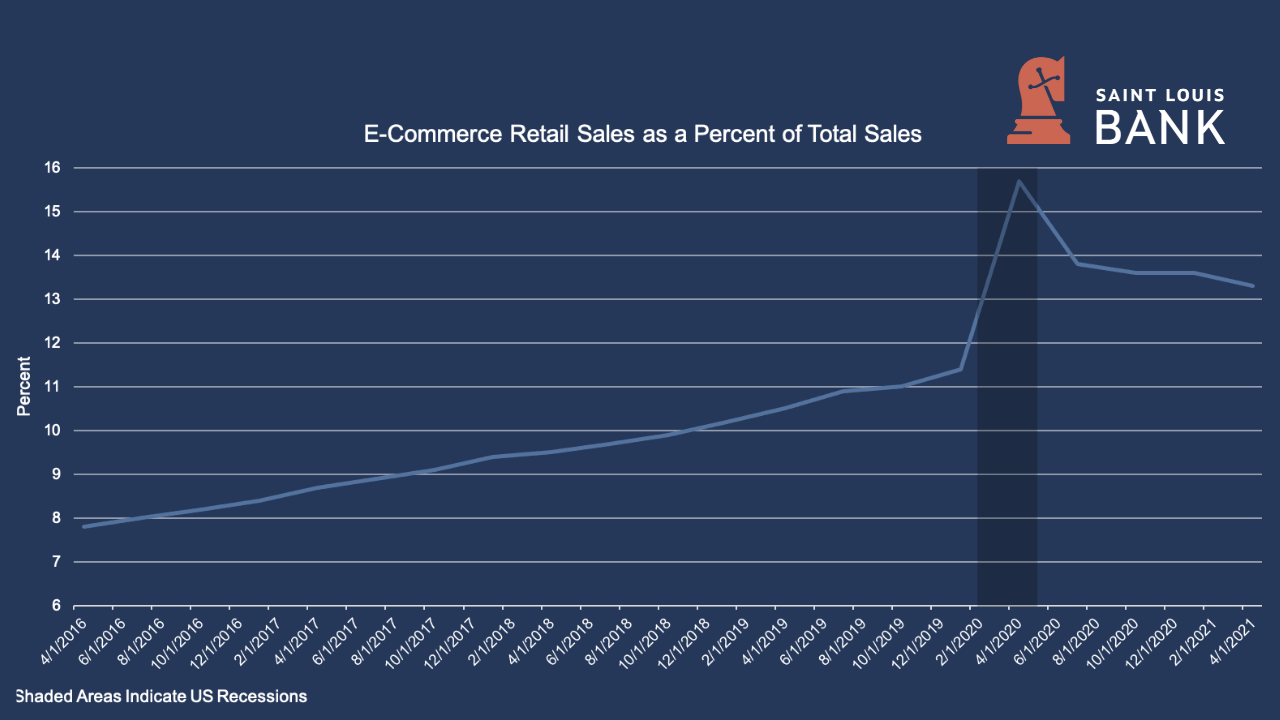

The Federal Reserve Bank of St. Louis’ “e-commerce retail sales as a percent of total sales” data as illustrated in the graph below shows the material increase in online sales during the pandemic. While it is expected that e-commerce sales will remain high, there has been a leveling off as vaccines are distributed and restrictions lifted.

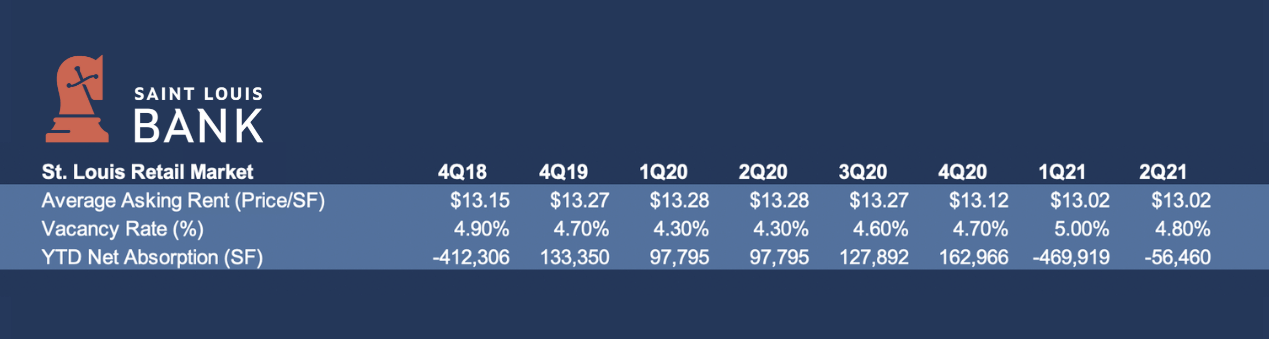

The overall St. Louis retail market loosened year-over-year in the second quarter of 2021, realizing a 30-basis point increase in vacancy to 4.8%. Net absorption totaled 73,899 square feet for the past four quarters and 514,863 square feet for the past two years. The average quoted rental rate is $13.02 per square foot, down $0.15 per square foot from one year ago.

In the local retail market:

——————————————————————————–

Data Sources: Newmark Zimmer St. Louis Industrial Market Research Report Q2 2021; Newmark Zimmer St. Louis Office Market Research Report Q2 2021; Newmark Zimmer St. Louis Retail Research Report Q2 2021; Denver University – Burnes School of Real Estate & Construction Management – Real Estate Market Cycle Monitor – First Quarter 2021; FRED Economic Data – Federal Reserve Bank of St. Louis.

Disclaimer: The views and opinions expressed are those of the authors and do not necessarily reflect the official policy or position of Saint Louis Bank. Any assumptions made in the analysis are not reflective of the position of any other entity other than the author(s), and since we are critically-thinking human beings, these views are always subject to change, revision, and rethinking at any time. The information contained within has been obtained from sources we believe to be reliable; however, we have not conducted any investigation regarding these matters and make no warranty or representation whatsoever regarding the accuracy or completeness of the information provided. While we do not doubt its accuracy, we have not verified it nor make any guarantee, warranty or representation of any kind or nature about it. The use of or reliance upon and resource provided is a tacit acceptance that the reader understands that the materials may be out of date, opinion-based, incorrect, or biased. It is the reader’s responsibility to verify their own facts.

St. Louis Bank is an Equal Housing Lender and Member FDIC.