Business Banking

We have separated this month’s report into three sections: Industrial, Office, and Retail, to either consume the information that is most relevant to you or read fully. Each sector differs in its response to the COVID-19 pandemic. However, as a whole, we can see a region that is continuing to adapt to a year of unparalleled circumstances.

The industrial sector entered the pandemic on solid footings, and while there have been pockets that have been adversely affected, the industrial market has been one of the most resilient real estate sectors amid the COVID-19 pandemic. This resiliency has been largely driven by changing consumer behavior, particularly in e-commerce growth. It is anticipated that industrial space will continue to be active as consumers demand rapid delivery of more products and manufacturing activity picks up.

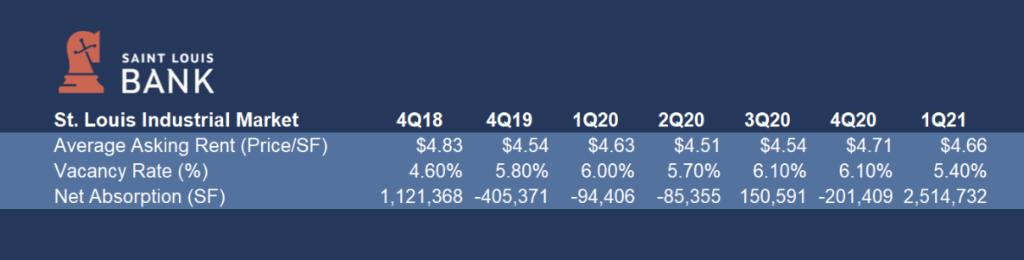

The St. Louis industrial sector tightened in the first quarter of 2021. During this period, the market realized positive absorption of 2.5 million square feet, the largest quarterly absorption since third-quarter 2017. Overall vacancy decreased 70 basis points from the prior quarter to 5.4%, while average quoted rents decreased from $4.71 per square foot to $4.66 per square foot. Three properties, the 154,940 square foot Soulard Commerce Center, the 34,000 square foot flex property at 2878 Telegraph Road, and the 33,000 square foot building located at 700 Fountain Lakes Boulevard delivered 221,940 square feet of product to the market during the quarter, while developments under construction increased to 2.7 million square feet of product planned for delivery.

The market picked up pace during the quarter. However, net absorption totaled 3.1 million square feet for the past four quarters, equating to a 24.0% decrease from the annual average net absorption of 4.1 million square feet during the previous five years. Quoted rental rates increased by $0.09 per square foot over the past year. With market vacancy at 5.4%, the following major projects are currently under construction. It should be noted that speculative construction accounted for nearly 70% of the development pipeline evidencing investors’ bullish sentiment on the industrial market in the St. Louis MSA.

The St. Louis industrial market is well-positioned for the remainder of 2021 as emerging Midwestern industrial markets, including St. Louis, Kansas City, Memphis, Indianapolis, Nashville, and Columbus, continue to attract significant investments, as well as user activity. The industrial market’s strong prevailing fundamentals, coupled with reasonable rental rates, an affordable workforce, and centralized geographic locations, will continue to attract new tenants in the Metro looking to invest heavily in logistics and industrial networks. A more pronounced shift toward online retail will increase demand for warehouse and distribution space, especially in fringe or ex-urban locations, such as St. Charles County and North County, with last-mile facilities possessing greater importance in the market as demand continues to rise in 2021.

The significant pandemic-driven changes to the office sector last year will carry into 2021 and beyond, as companies adapt innovative new operating models. Buildings emptied last year as companies downsized and shifted their staff to working from home. To meet health and safety standards, facility operators quickly enhanced their cleaning procedures, upgraded HVAC systems, erected plexiglass barriers, closed shared spaces, and added other physical-distancing measures to keep workers safe. Companies have become increasingly nimble, adding sophisticated remote-work capabilities. Most companies have effectively halted their office space expansion plans, shelving growth strategies until the vaccine reaches a critical mass of the population and clarity on the future of office work emerges.

Most firms recognize there is always going to be a need for office space. However, it may be less dense and/or more flexible to accommodate hybrid work from home models. The more crucial determinant of office demand is sheer job growth.

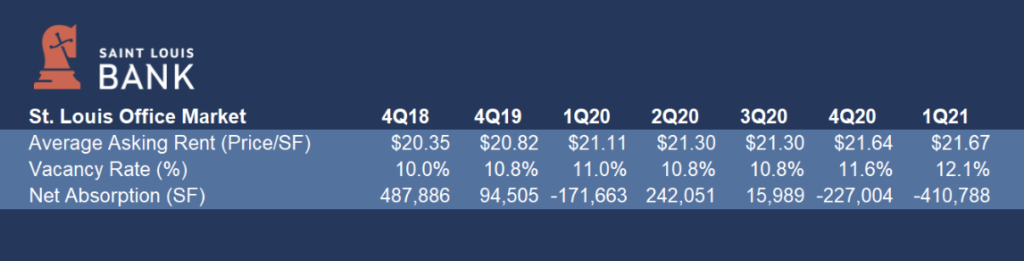

The St. Louis office market realized a slight increase in asking rental rates in the first quarter of 2021, as rents climbed to a record high of $21.67 per square foot, up $0.03 per square foot from the fourth-quarter 2020. Market vacancy rose to 12.1%, an increase of 50 basis points from the prior quarter and an increase of 120 basis points from one year ago. Total net absorption in the quarter measured negative 410,788 square feet, bringing the total for the past four quarters to negative 766,666 square feet. One construction project underway during the quarter totaled 224,585 square feet. The Class A, Forsyth Pointe project in Clayton is currently 41.7% pre-leased. A total of 108,750 square feet delivered to the market as the Edge@West, Class A property in Mid-County officially finished construction.

The relatively low level of new construction activity tells only part of the story. Across the St. Louis region, there has been a spike in sublet inventory. Since year-end 2019, the amount of space available for sublease increased by roughly 692,000 square feet or about 140% as firms downsized leased space. With increased sublease activity expected to continue, discounted inventory will force landlords to reconsider current pricing on direct space, leading to potential compression in asking rates as office markets navigate the pandemic. That said, leasing commitments during 1Q21 were active in various submarkets as tenants locked in favorable terms for new direct and subleased spaces, as well as renewals. It is believed that these more favorable terms may be a residual impact from COVID-19 and the overall stresses on the office sector. Users in the healthcare and government sectors led the quarter, including Stereotaxis, Inc.’s lease in Downtown St. Louis, the State of Illinois Department of Central Management Services’ lease in Belleville, The Federal Public Defender’s renewal in Downtown St. Louis, CAS Group, LLC’s lease in Clayton and Luxco’s lease in West County. Expect favorable conditions and multiple opportunities for prospective tenants in the market to upgrade from Class B or B+ space to Class A space in 2021, as most submarkets in the Metro display vacancy rates for Class A space ranging from 9.3% to 13.8% with vacancy in North County and Downtown St. Louis of 21.0% and 25.8%, respectively. Overall market vacancy should range from 11.8% to 12.8%, while asking rental rates are expected to range from $20.60 per square foot to $21.85 per square foot during the next four quarters.

Spark St. Louis, a locally based coworking concept created by the St. Louis Cardinals and The Cordish Companies, announced in February that it plans to open a 30,000 square foot space in the 127,000 square foot PwC Pennant Building within Ballpark Village in Downtown St. Louis. Delivered to the market in October 2019, the Class A property will house The Cordish Companies’ third collaborative workspace community, following Spark Baltimore in 2016 and Spark KC in 2020. Located at 6 Cardinal Way, Spark Coworking will offer 24-hour access, mailbox and concierge mail service, a kitchenette, member events, including happy hours, private phone call areas, a podcast studio area, an outside terrace, and an on-site mothers’ room and wellness space. The space will include more than 80 private offices, five suites, and dedicated and non-dedicated workstations with the ability to reserve space on a daily or monthly basis. Private office rates are currently quoted at $595 per month, with workstation memberships priced at $225 per month. Daily passes are $15 per day for non-members. Spark Coworking is expected to open in mid-2021.

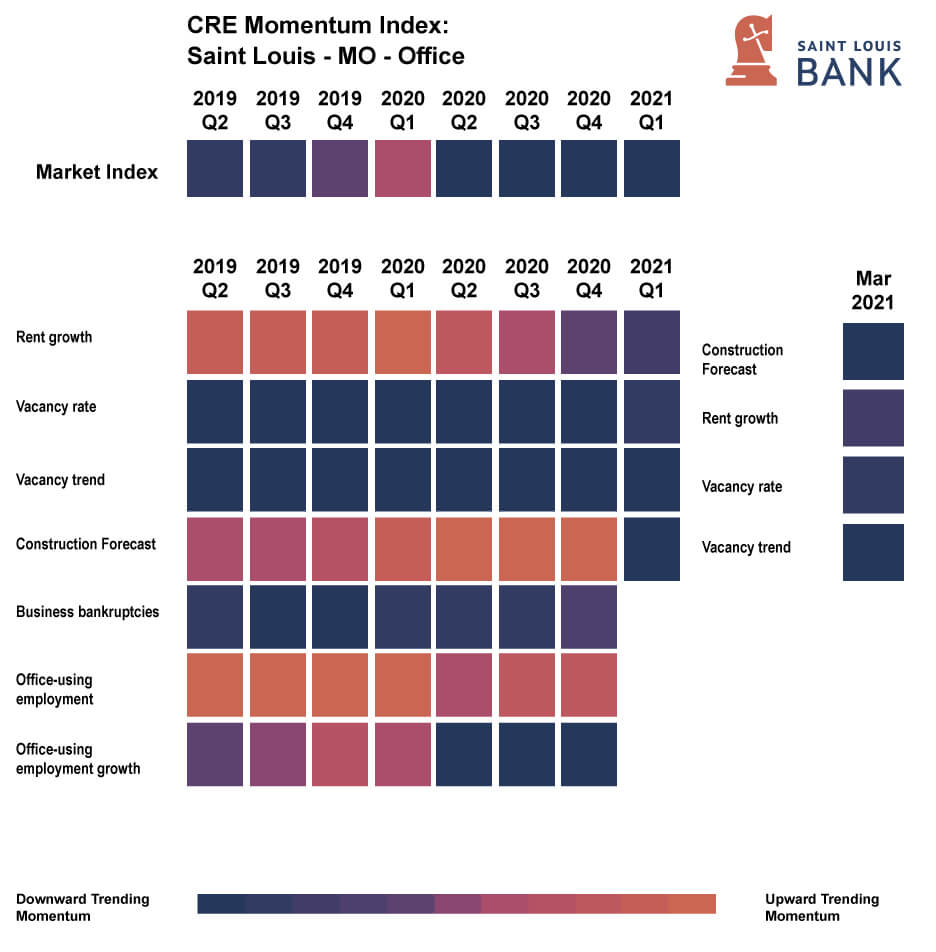

The following provides summary data available from the Federal Reserve Bank of Atlanta featuring their “Commercial Real Estate (CRE) Momentum Index.” This index provides a time series analysis of numerous market dynamics which are aggregated to help understand the momentum of change in commercial real estate markets across the country. The table below includes the Momentum Index for the St. Louis office market and is used to assess emerging risks. Orange hues indicate a value above the average (“upward”) and blue hues indicate a value below the average (“downward”). Mauve hues reflect data that are in line with the long-term average. As shown, there are consistent risks noted in various factors relating to the office market.

The retail sector is unsurprisingly expected to be the hardest hit of all real estate sectors, as government mandates ordered the closure of non-essential businesses in almost every state. As it is predicted that more than half of job losses to come will be in the services sector, the more dire outcome scenarios are expected to be realized in retail space. More retailers went bankrupt in 2020 than during the Great Recession – especially department stores and apparel retailers. As brick-and-mortar retailers burn through cash reserves and consumers shop online even more, retail properties will go empty in the first half of 2021. Experts predict there will be 20% less retail real estate by 2025. There will continue to be demand for retail space particularly as the coronavirus vaccine is distributed, but this space may look different as sales will be fueled by more than pedestrian traffic, including curbside pick-up and same-day delivery for food consumption, household items, and personal needs. The short-term shift in consumption caused by the pandemic is set to transform into a widespread and long-term retail shift in consumer shopping behavior in the U.S.

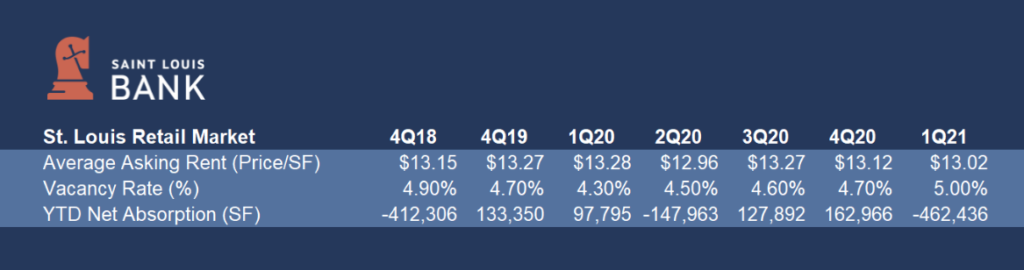

The overall St. Louis retail market loosened year-over-year in the first quarter of 2021, realizing a 60-basis point increase in vacancy to 5.0%. Net absorption totaled negative 590,046 square feet for the past four quarters and 301,929 square feet for the past two years, indicating a slowing market. The average quoted rental rate is $13.02 per square foot, continuing a downward trend.

In the local retail market:

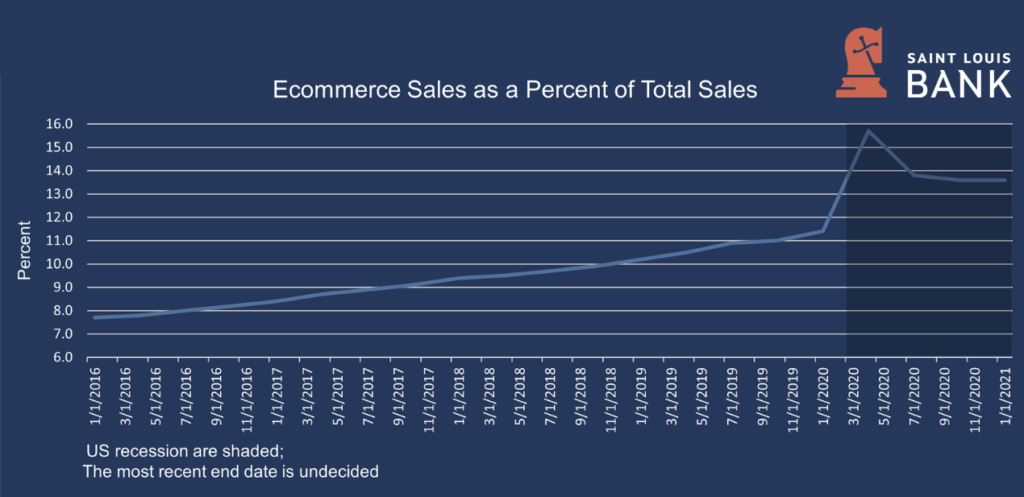

In response to COVID-19, many retailers had to adopt different business models with the transformation continuing based on consumer preferences. The Federal Reserve Bank Economic Data (FRED) shows a material increase in online sales during the pandemic as evidenced by the level of e-commerce retail sales as a percent of total sales. It is expected that this upward trend will continue, in part due to the increase in confidence in online purchasing through mobile devices from non-millennials. In 2021, the shift towards online retail purchasing is expected to accelerate further as small to mid-sized retailers with little or no online presence are allocating resources to capture e-commerce sales. This industry trend will impact many retail property tenants. The vaccine does provide light at the end of the tunnel. Demand for restaurants could soar and choices for diners will be more limited after restaurant closures due to the pandemic. Many could be challenged, however, with staffing shortages.

Mall traffic had been on a downward trend long before the pandemic turbocharged online shopping. Anchors such as J.C. Penney and Macy’s are liquidating hundreds of locations to right-size in the wake of a shift in demand. Gap also recently announced plans to close all its mall-based stores. Other traditional mall retailers have also shuttered completely, including GNC. These moves will leave many of these properties with an insufficient base of retailers to continue operating due to decreased traffic. Mall vacancy has jumped more than 100 basis points since the end of 2019, the largest rise across all retail concepts. Locally, the Chesterfield Mall is slated for demolition to be replaced with a mix of multifamily apartments, offices, retail, entertainment, and green space. This development called “Downtown Chesterfield” is being led by The Staenberg Group. Centers with grocers are set to outperform, and convenience stores and casual dining restaurants are poised for recovery.

Data Sources: FRED Economic Data; Newmark Zimmer St. Louis Industrial Market Report Q1 2021; Newmark Zimmer St. Louis Office Market Report Q1 2021; Cushman & Wakefield Marketbeat – St. Louis Office Q1 2021; Newmark Zimmer St. Louis Retail Report Q1 2021; Federal Reserve Bank of Atlanta – Commercial Real Estate Momentum Index.

Disclaimer: The views and opinions expressed are those of the authors and do not necessarily reflect the official policy or position of Saint Louis Bank. Any assumptions made in the analysis are not reflective of the position of any other entity other than the author(s), and since we are critically-thinking human beings, these views are always subject to change, revision, and rethinking at any time. The information contained within has been obtained from sources we believe to be reliable; however, we have not conducted any investigation regarding these matters and make no warranty or representation whatsoever regarding the accuracy or completeness of the information provided. While we do not doubt its accuracy, we have not verified it nor make any guarantee, warranty or representation of any kind or nature about it. The use of or reliance upon and resource provided is a tacit acceptance that the reader understands that the materials may be out of date, opinion-based, incorrect, or biased. It is the reader’s responsibility to verify their own facts.

St. Louis Bank is an Equal Housing Lender and Member FDIC.