Business Banking

The industrial sector entered the pandemic on solid footings, and while there have been pockets that have been adversely affected, it has been one of the most resilient real estate sectors amid the COVID-19 pandemic. This resiliency has been largely driven by changing consumer behavior, particularly in e-commerce growth. It is anticipated that industrial space will continue to be active as customers demand rapid delivery of more products and manufacturing activity picks up.

Warehouses were the unexpected champion of commercial real estate during the pandemic, and their success is expected to continue into 2021 as logistics companies try to catch up with the demand for e-commerce orders.

Since 2017, St. Louis has recorded 24.0 million square feet of positive absorption within the industrial market, accounting for nearly 9.3% of inventory.

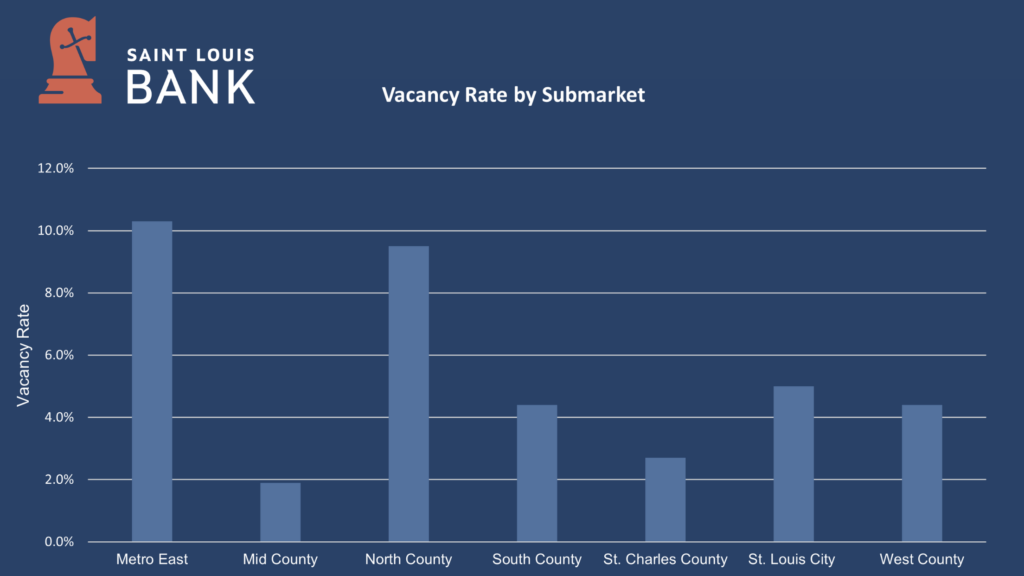

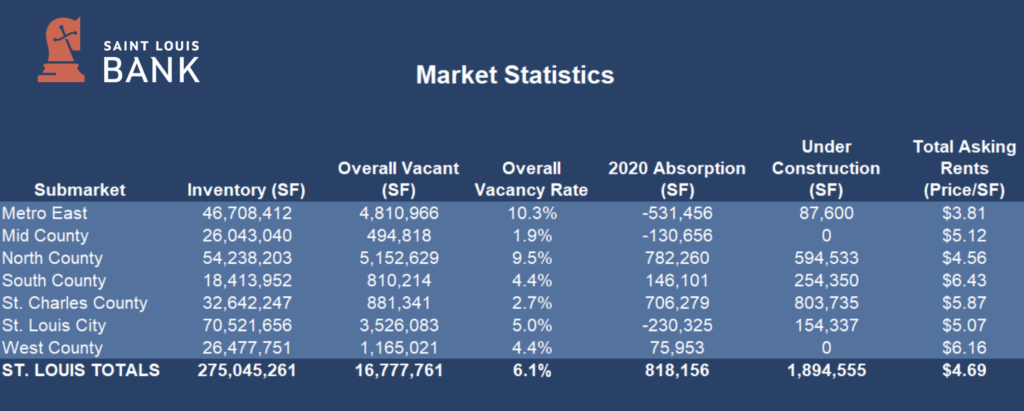

For the fourth quarter of 2020, overall vacancy rates for industrial space increased 10 basis points from the prior quarter to 6.1%, while average quoted rents increased from $4.63 per square foot to $4.69 per square foot. Vacancy was up 50 basis points year over year. Asking rents varied by submarket with the Metro East on the low end at $3.81 per square foot while West County was at the upper end at $6.16 per square foot. The median asking rental rate was reported in Mid County at $5.12 per square foot. During the quarter, the market realized negative absorption of <365,626> square feet with net absorption for the past four quarters totaling 818,156 square feet. Asking rental rates have increased in 18 out of the past 24 quarters with positive net absorption occurring in 24 out of the past 29 quarters.

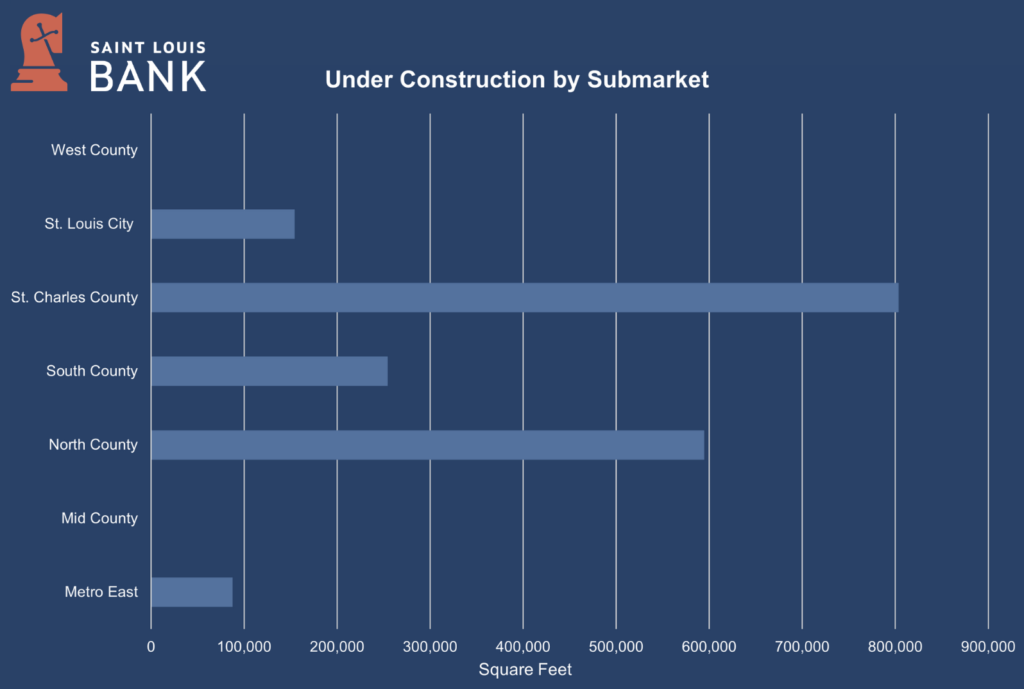

Two properties, the 543,227 square foot Gateway TradePort 2 in Pontoon Beach, IL, built on a speculative basis, and the 240,000 square foot building at 521 Pearl Drive, O’Fallon, MO (100% leased to Cosmos Corporation), delivered 783,227 square feet of product to the market during the quarter, while developments under construction decreased to 1.9 million square feet of product planned for delivery.

The global health crisis prompted by COVID-19 has left an indelible mark on society, structurally changing how people live, work, and play. The dramatic lifestyle changes of the last 12+ months will directly affect the supply and demand characteristics of all types of commercial real estate – both over the short-term and long-term. The following are considered tailwinds for industrial growth as we near the beginning of the second quarter of 2021.

In St. Louis, the industrial market is well-positioned in the manufacturing, distribution, and logistics sectors for any COVID-19 shifts due to its adaptable workforce, geographically centralized locations, multi-modal transportation network, and affordable real estate costs. The ability to service various facets of the supply chain all from one metro area will become essential as supply chains become shorter. A more pronounced shift toward online retail will increase demand for warehouse and distribution space. Developers will likely continue to seek opportunities in more fringe or exurban locations; those with multi-modal access will be the most desirable. Last-mile facilities will possess even greater importance in the market as demand continues to rise.

Data Sources: Newmark Zimmer St. Louis Industrial Market Report Q4 2020; Cushman & Wakefield Marketbeat St. Louis, Industrial Q4 2020; Marcus & Millichap U. S. Commercial Real Estate Investment Outlook

Disclaimer: The views and opinions expressed are those of the authors and do not necessarily reflect the official policy or position of Saint Louis Bank. Any assumptions made in the analysis are not reflective of the position of any other entity other than the author(s), and since we are critically-thinking human beings, these views are always subject to change, revision, and rethinking at any time. The information contained within has been obtained from sources we believe to be reliable; however, we have not conducted any investigation regarding these matters and make no warranty or representation whatsoever regarding the accuracy or completeness of the information provided. While we do not doubt its accuracy, we have not verified it nor make any guarantee, warranty or representation of any kind or nature about it. The use of or reliance upon and resource provided is a tacit acceptance that the reader understands that the materials may be out of date, opinion-based, incorrect, or biased. It is the reader’s responsibility to verify their own facts.

Saint Louis Bank is an Equal Housing Lender and Member FDIC